Corporate Climate Commitments: Empty Promises or Profit-Driven Strategy?

The surge of corporate climate pledges worldwide raises a fundamental question: Are these commitments the latest incarnation of cheap talk and greenwashing, or could they meaningfully accelerate decarbonization, even if firms are purely profit-driven? The 2015 Paris Agreement marked a turning point in climate negotiations, with nearly 200 nations committing to achieve “Net Zero” greenhouse gas emissions by 2050. Effective climate policy requires addressing a dual externality: not only should carbon emissions be taxed to mitigate climate damages directly, but green innovation should also be subsidized to take advantage of technological spillovers between firms and minimize the economic costs of decarbonization. Indeed, recent empirical work sheds some light on the appropriate policy mix: innovation subsidies could be efficient for innovation incentives, but green innovation alone, without carbon pricing, fails to reduce emissions. These findings reinforce the theoretical argument for policy complementarity. Yet government pledges to date lack specific enforcement mechanisms, and governments have struggled to implement credible long-run climate policies, in part due to extreme political uncertainty. The need for an efficient policy mix makes the lack of government credibility especially concerning.

Against the backdrop of such uncertainty, an unexpected group has emerged as catalysts for change: large corporations and institutional investors. The scale of private sector engagement is remarkable: global data from the Science Based Targets initiative (SBTi) shows that over 1,200 firms had made Net Zero commitments between 2016 and 2023.

In Acharya, Engle and Wang (2024), we ask fundamental questions that arise from observing this surge in private sector climate commitments: Are these long-term commitments best viewed as meaningless posturing, or could they have a real impact on decarbonization? What is driving firms to commit? Is the main objective to please climate-conscious stakeholders even if following through hurts companies’ bottom line, or could firms and investors actually profit from making such commitments? And how do these private initiatives interact with government climate policies? To answer these questions, we develop a model of firms’ choices over production, emissions, and green innovation or technology adoption in an economy with two key market failures: environmental damages from carbon emissions and technological spillovers where social returns to green innovation exceed private returns.

We find that even profit-motivated large firms and institutional investors can and should use commitments to accelerate the green transition when government climate policies face constraints. In our model, firm commitments are defined as “over-investments” in green innovation and technology adoption relative to a standard decentralized equilibrium, because cleaner technology is the only credible way committing firms can ensure reaching low emissions. The key mechanism works through technological spillovers: when some firms commit to decarbonize, they reduce the costs of clean technology adoption for all firms in the economy. This strategy benefits committing firms even if they are purely profit-maximizing, by lowering their own cost of decarbonization and transition risk. Most surprisingly, private commitments reduce pressure for future carbon taxes, thereby enhancing the credibility of government climate policies.

This insight resolves an apparent puzzle in climate policy. In an ideal world with perfect policy instruments – both carbon taxes and innovation subsidies – private commitments would be unnecessary. But assuming that the space of policy instruments is rich enough to address the multitude of externalities in managing climate change ignores the different constraints faced by different countries. For instance, the policy at present in Europe is focused more on measuring total emissions and taxing them, rather than measuring green innovation that lowers emission intensity and incentivizing it; the opposite holds in the U.S., with the Inflation Reduction Act of 2022 introducing substantial green innovation subsidies (aimed at reducing emission intensity) but no carbon pricing.

In this second-best world, large firms and institutional investors can help fill the gap. Firm size matters because any individual small firm is too insignificant to affect others’ incentives. But sufficiently large firms can act as “Stackelberg leaders”: by moving first with ambitious commitments, they trigger a virtuous cycle of investments in green technology reducing costs for others, spurring broader adoption and ultimately lowering carbon tax bills for everyone – including themselves. This description makes clear that the firms making commitments must be acting non-atomistically, in the sense that they realize their actions can shift the equilibrium. This can take the form of commitments by “large” firms, but also by “green common ownership”, that is, coalitions of firms owned by large institutional investors belonging to a common climate alliance, taking into account positive spillovers in green innovation at the combined portfolio level.

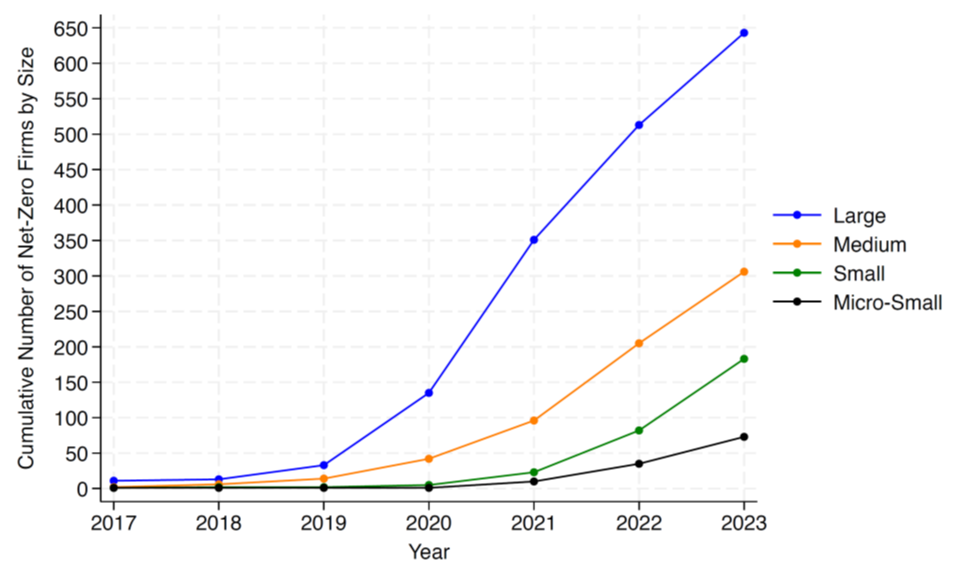

Figure 1: Cumulative number of firms having made a Net Zero commitment by firm size

[Note that firm size is measured by assets: “Large” ($10 billion or more), “Medium” ($2 billion to $10 billion), “Small” ($250 million to $2 billion), and “Micro-small” ($250 million or less).]

The data on firm commitments supports this mechanism. Figure 1 illustrates that large firms consistently led their smaller counterparts in making these commitments between 2016 and 2023. Commitment rates increase first for large firms, then medium firms, and finally smaller firms. This is exactly what we would expect technological spillovers rather than common shocks or industry trends, which would likely affect all size categories simultaneously. Further empirical analysis shows that large firms in both the US and elsewhere have made (earlier) Net Zero commitments and undertaken (earlier) decarbonization investments. This is the case also for “green common ownership”, defined as firms in the US owned more by large institutional investors (as reported in 13F SEC filings) who have themselves made Net Zero commitments. While common ownership is often criticized for potential anti-competitive effects, our analysis reveals an unexpected bright side of (green) common ownership in the presence of technological spillovers.

Crucially, our theory does not require firms to be environmentally motivated. The prospect of future carbon taxes creates purely financial incentives for large players to move first. The only reason these firms commit is to ultimately reduce their carbon tax burden. This carbon tax-saving motive highlights an important asymmetry in terms of constrained public policies. We show that firm commitments have large welfare benefits in countries with carbon taxes but constrained innovation subsidies, because taxes are where firms stand to save the most by committing. By contrast, firm commitments do not improve welfare as much when unconstrained innovation subsidies are available, but carbon taxes are infeasible in the foreseeable future. In that case, the subsidies already incentivize innovation, whereas commitments bring no additional carbon tax-saving. Importantly, it is not the current carbon taxes and pricing that matters, but the expected path over the next decades, which is often referred to as “transition risk”.

Perhaps our most striking finding is that private commitments not only help fill policy gaps, but also make government commitments more credible. We model government commitments as promises of future carbon taxes. This is analogous to the concept of “forward guidance” in monetary policy, but applied to climate policies. Here’s how it works: governments may want to commit to future stringent climate policies because the anticipation of a carbon tax above and beyond the social cost of carbon stimulates ex-ante green innovation, as firms seek to reduce their future carbon tax bill. Promising a high carbon tax therefore acts as an imperfect substitute for any missing green innovation subsidy. However, a carbon tax exceeding the social cost of carbon will turn out to be excessively high ex post, once green technology investments have been sunk, and the future government will be tempted to lower the carbon tax back to the social cost of carbon.

Private commitments help resolve this time-consistency problem. When firms shoulder more of the green transition burden, governments don’t need to threaten stringent policies to achieve their goals. Surprisingly, this makes their policy commitments more credible, since the temptation to renege is lower. The reason governments make commitments is to provide ex-ante for green innovation when the private sector fails to internalize technological externalities. Firm commitments perform the same function, and therefore stronger firm commitments reduce the need of the government to promise high future carbon taxes, thereby making the government’s promises more credible. In other words, in a world where government commitments to climate policies are likely to be weak, large firms and common ownership emerge as being paramount in shepherding the green transition. While some firms and banks have recently pulled out of climate alliances, particularly in the U.S., this pattern actually supports our framework. Our analysis underscores that profit-driven firm commitments require some credible expectation of future carbon pricing. The weakening political support for carbon pricing in the U.S. naturally reduces firms’ incentives to commit. Moreover, the substantial green innovation subsidies now in place through the Inflation Reduction Act have made firms’ strategic role in spurring innovation less essential. This contrasts with Europe, where carbon pricing is more credible but innovation subsidies remain constrained, making firm commitments more valuable.

Our findings have important implications for policy design:

- Carbon pricing and emission caps remain essential, because transition risk provides the underlying incentive for firms to commit. However, this relationship works both ways: governments can achieve their goals with less stringent policies when private commitments are widespread.

- Private initiatives work best in jurisdictions with more constraints on innovation subsidies than on carbon pricing, because firms’ incentives to reduce their carbon tax bill is stronger.

- Regulators should be cautious in how they view coordination among firms on climate issues. While antitrust concerns about common ownership are valid, some degree of coordination is valuable to accelerate decarbonization, by allowing firms to internalize technological spillovers.

Private commitments aren’t a panacea. They can’t fully substitute for government policy, and their credibility ultimately depends on anticipated future carbon prices. But in a world of constrained policy instruments, large firms and institutional investors can serve as powerful catalysts for the green transition. The key insight is that effective climate action doesn’t rely solely on corporate altruism. Instead, rational anticipation of future policy and recognition of technological spillovers can go a long way.

Distribution channels: Education

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Submit your press release